A fixed cost doesn’t change with the level of output or activity in the short run. Insurance premiums, license fees, lease payments, and administrative salaries all keep accruing whether the plant makes 1 widget or 10,000. They’re tied to having the operation, not to running it.

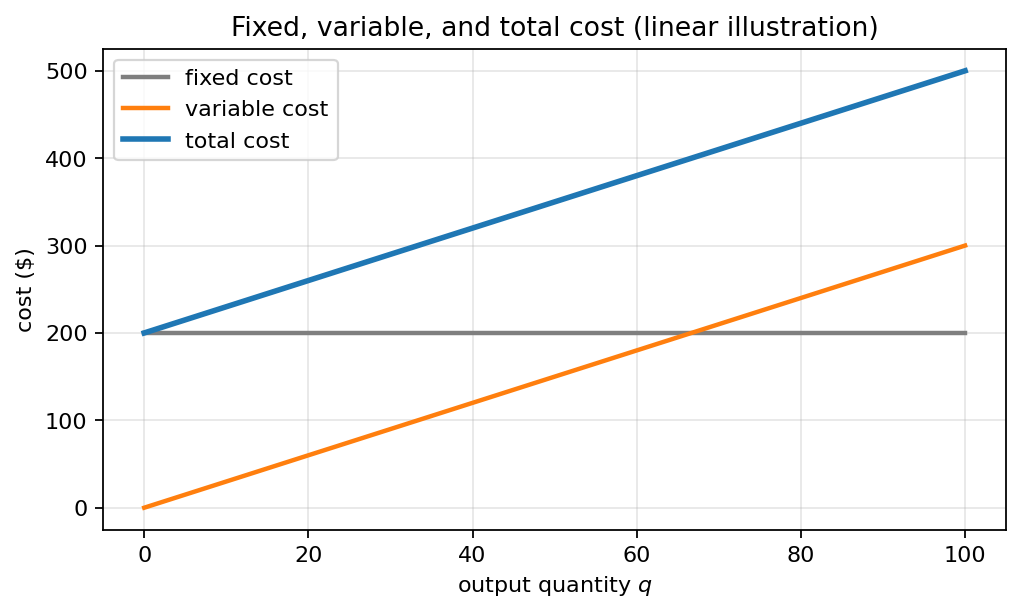

Fixed, variable, and total cost as a function of output.

Fixed, variable, and total cost as a function of output.

Fixed costs contrast with variable costs, which scale with output (labour-hours, raw materials, electricity to drive machines). Most real businesses have a mix: a total cost curve is , where is fixed and grows with the quantity produced .

The fixed/variable split drives break-even analysis and the operating-leverage discussion in business planning. A business with high fixed costs (factories, fleets, datacentres) is very profitable once revenue clears the break-even line but very fragile below it, since every unit unsold still costs the fixed amount. A business with mostly variable costs (consultancies, marketplaces) is the opposite: lower upside per unit, lower downside if demand falls.

Fixed only in the short run. Given enough time every cost is “variable”: a company can sublease the building, terminate the lease, cancel the insurance. The line between fixed and variable shifts with the time horizon.